YOUR BUSINESS AUTHORITY

Springfield, MO

YOUR BUSINESS AUTHORITY

Springfield, MO

By: Ashlee Radford, Industry Insight

By: Ashlee Radford, Industry Insight You’ve certainly heard some variation of the cliche “make your money work for you.” It permeates marketing efforts across industries, makes a catchy headline and speaks to our desires to be not just successful but also thriving.

As business owners, managers or even stewards of public funds, that’s especially true. These large depositors often have funds sitting in accounts that either earn zero interest or exceed the maximum amount of insurance protection by the Federal Deposit Insurance Corp. Put simply, these large deposits could be doing much more. They could be working smarter.

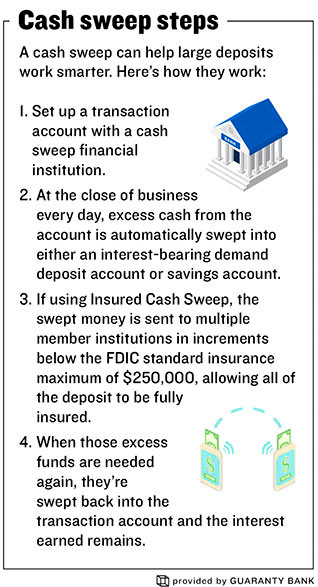

The solution is a cash sweep product. If you’ve never checked into it, the premise is pretty simple: Excess cash is taken from one account at the close of each business day and “swept” into another account automatically, one that earns higher interest. Because sweep accounts maintain liquidity, that cash can be swept back when it’s needed, but it’s garnered that higher interest rate in between.

Several cash sweep options exist on the market, but my favorite might be Insured Cash Sweep because, unlike some, it provides protection for funds beyond the $250,000 FDIC maximum. Here’s how: When an ICS-member bank places your funds in ICS, that deposit is sent from the transaction account to deposit accounts at other ICS network financial institutions in amounts below the standard FDIC threshold. As a result, all of the funds are eligible for millions of dollars in FDIC insurance, and no one in history has ever lost a penny of FDIC-insured deposits. For small businesses, that kind of peace of mind can be invaluable.

Regular monthly statements from your relationship institution keep things simple. There’s no need to track collateral on an ongoing basis, footnote uninsured deposits, manage multiple banking relationships or manually consolidate bank statements. This can make it a fantastic time-saver.

No matter which cash sweep product selected, earning interest while maintaining access to these liquid funds is the heart of it. Interest rates often can be negotiable, whether you’re using demand deposit accounts or even CDs with quick maturities. There are plenty of options that can be tailored to your particular cash-flow needs, while many allow for unlimited program withdrawals for funds in demand deposit accounts or a set number for savings accounts. Interest earned comes back to you in consolidated payments, so you can use them however you like or continue to grow the excess funds.

Sweep accounts aren’t just for businesses, either. Public funds for local governments, schools, police departments, hospitals, utilities and more can be swept into interest-bearing demand deposit accounts or money market deposit accounts that are eligible for FDIC insurance. This can make it simple to both earn a return and protect the public’s vital resources.

Finding a relationship with an ICS member institution can be quick and easy. There are more than 20 financial institutions in the state of Missouri offering the service, with several hundred more across the country. The American Bankers Association also endorses ICS, citing how it helps banks attract large-dollar deposits that can be used for lending in their local communities, and utilizes beneficial alliances with the Independent Community Bankers of America and Community Development Bankers Association.

So why let your excess money sit idle in a single account that may not be backed by the full faith of the U.S. government, earning little or no interest? You have options to sweep that money into an account that more literally works smarter.

Ashlee Radford is the director of corporate services at Guaranty Bank in Springfield. She can be reached at aradford@gbankmo.com.

A safe room and classroom addition at Willard Central Elementary School will be used by the music, arts and athletic programs for a district that had 4,536 students last year, according to Missouri Department of Elementary and Secondary Education figures, but school officials say enrollment is projected to grow.