YOUR BUSINESS AUTHORITY

Springfield, MO

YOUR BUSINESS AUTHORITY

Springfield, MO

BY: Dylan Holloway

BY: Dylan Holloway “Well, now what?”

People will ask this question from time to time, usually when reaching the end of something and feeling no direction. This can be particularly true when reaching the endpoint in one’s career and considering retirement. People consult their spouse, children and financial adviser, as well as their human resources department, to receive guidance on departing their position.

But what do farmers do?

They either keep going or sell out.

They don’t have set guidelines for retirement. Most times, they don’t have a 401(k) or a pension. Their retirement plan is invested in livestock, equipment and real estate, and the key to start drawing their retirement is by marketing these assets as efficiently as possible. Well, now what? For those with family members willing and able to take over the farm operation, a succession plan needs to be in place.

There are several arrangements that can be put together in which the new owner makes payments and/or shares their produced commodity with the selling individual. Owner financing is a great way to transition farm assets because it can remove the need for a sizeable down payment and greatly reduce the tax liability for the seller.

If owner financing is not feasible, there are several state and federal government programs available that will work in conjunction with bank financing. There are programs available to beginning farmers, as well as those looking to expand their operations. Selling to family is the most ideal situation, as it allows the farm structure to stay intact – and it lets another generation continue the traditions of the family operation.

Those without family to buy the farm have a lot of options and resources for selling out. The most desirable situation is selling the entire farm and all equipment as a package deal with a single, all-inclusive price. I have seen this successfully take place, and it makes for the smoothest process, in my opinion.

I advise those looking to sell out to consult with several individuals in order to make an informed decision. Your accountant or tax preparer, financial adviser, banker, livestock auction field representatives, equipment dealers, auctioneers and your University of Missouri Extension agent are great places to start. A well-thought-out plan will yield the best return and position one financially better than a quick auction or dispersal.

But those who aren’t quite ready to let go and sell out may be the most valuable. They have great opportunities to take someone under their wing – a neighbor, son or daughter, grandson or granddaughter, a friend or a hired hand. These individuals are the future and will be needed for farm production.

There are many creative ways to successfully involve people new to farming. Once enough experience is gained, sell them a few cows with the expected repayment coming from milk or calves. Rent them equipment and a crop field, and split the harvest. Empowering these individuals as they gain knowledge and earn responsibility may be the best way to keep them interested and wanting to do more.

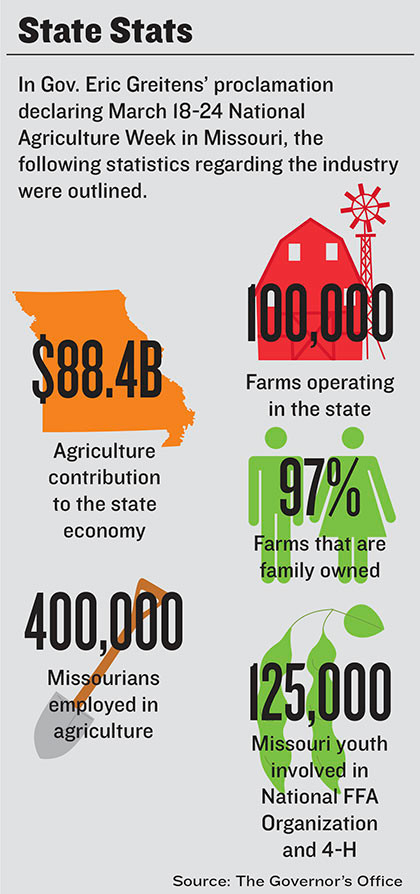

The average age of Missouri farmers is 58 years old, according to the National Agricultural Statistics Service – an increase from 54 years in 1997. When considering the majority of farmers fall into the 45-54 and 70-plus age groups, it is time to start considering these options and planning for your future as well as the next generation. Agriculture is an $88 billion industry, employing nearly 400,000 people, according to the Missouri Department of Agriculture.

Let’s keep it that way.

Dylan Holloway is a commercial lender with OakStar Bank. He can be reached at dholloway@oakstarbank.com.

Alair Springfield is first Missouri franchise for Canada-based company.